Bank reserves and the falling loan to deposit ratio at US banks

By Sober Look

Earlier this week, CNN Money ran a story on JPMorgan’s quarterly results. Instead of focusing on the earnings, the author’s (Stephen Gandel) discussed the fact that JPMorgan’s loan-to-deposit ratio (LTD) hit a new low.

FORTUNE: – The nation’s largest banks are healthier than they have been in years. Someone, apparently, forgot to tell their loan officers.

JPMorgan Chase reported its 2013 profits on Tuesday. The news was mostly good — bottom line: $18 billion — but there was one significant black spot, not just for the bank, but for the economy in general. A key lending metric, the ratio of the bank’s loans-to-deposits, hit a new low.

In 2013, JPMorgan on average lent out just 57% of its deposits. That’s down from 61% a year ago and the lowest that ratio has been in at least a decade. Back in 2004, JPMorgan’s loan-to-deposit percentage was as high as 88%.

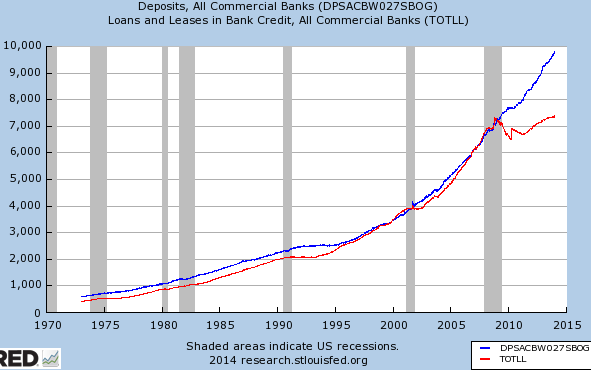

While JPMorgan’s LTD is particularly low, the bank is by no means unique. As discussed earlier (see post), LTD in the US is at the lows not seen in decades. On an absolute basis the gap between deposits and loans is now at some $2.4 trillion and growing. This divergence seems completely unique to the post-financial crisis environment.

|

| Red = loans and leases, Blue = deposits (all commercial banks) |

As the CNN story suggests, there are a few possible explanations for this trend. Here are four of them.

1. Demand for credit remains weak due to economic uncertainty, large amounts of cash on corporate balance sheets, jittery labor markets, poor wage growth expectations, general unease with taking on debt, etc.

2. Regulatory uncertainty and tighter (and to some extent unknown) capital requirements are preventing banks from extending more credit.

3. Exceptionally low rates make some forms of lending unprofitable.

4. Banks are running unusually large excess reserve positions with the Fed that are “crowding out” lending. These reserves are effectively “loans” to the Fed paying 25bp, funded with bank deposits that pay near zero, creating riskless profits with zero regulatory capital requirement.

There are arguments to be made for all four. The last one however is particularly intriguing because the $2.4 trillion gap between deposits and loans is a familiar number. The excess reserves in the banking system is now … also around $2.4 trillion.

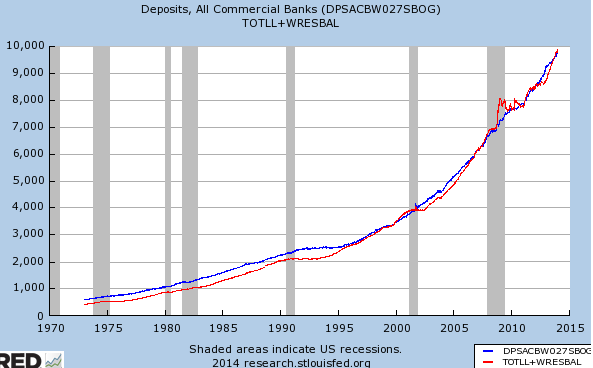

The chart below adds bank reserves held with the Fed to loans and leases – and the gap “disappears” (here we use total reserves vs. just the excess reserves, but the difference is not material to this trend.)

|

| Red = loans and leases + bank reserves, Blue = deposits (all commercial banks) |

Coincidence? Perhaps. But if there is any validity to the explanation #4 above, it would suggest that QE, which is directly responsible for the $2.4 trillion in excess reserves, was not helpful (and possibly harmful) to credit growth in the US.

Comments are closed.