What happens to banks’ balance sheets during a downturn?

By Sober Look

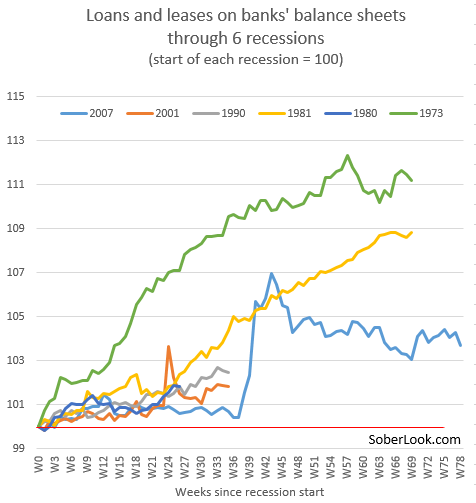

Credit underwriters pride themselves in their ability to cut lending when they sense that economic fundamentals have changed for the worse. For example one often hears bankers talking about passing on deals in 2007 because of “not liking the fundamentals” or “the markets looked stretched”. But historical data suggests otherwise. At least during the past 6 downturns, lenders increased balance sheets during the onset of each recession. And loan portfolios continued to grow, with lending often slowing only closer to the end of (and/or after) the recession.

|

| Above the red line (100) indicates an increase since recession’s start (source: FRB) |

But banks continue to insist that they will see the next recession coming and reduce exposure before the downturn. These “expected” balance sheet declines have been reflected in the stress tests that banks have been providing to the Fed, resulting in a more benign outcome. Given that the data clearly shows balance sheets rising, the Fed has decided to apply its own assumptions to how banks’ loan portfolios will change in the next downturn.

WSJ: – The Fed will now make its own projections about how bank balance sheets will fluctuate during a future recession, rather than rely on the banks for that data. The change is likely to produce different results in the 2014 tests, the Fed said. For instance, the central bank is likely to find bank assets will grow in a downturn, rather than contract as banks had projected in previous years. That could require firms to have more loss-absorbing capital or limit rewards to shareholders, though results will vary for each bank.

It seems that in reality, lenders (at least on average) tend to be terrible at calling the next downturn. And often by the time underwriting standards actually tighten, the worst of the slowdown is already over.

Comments are closed.