Britain’s illusory housing recovery

Apparently there is life in the UK housing market. According to ONS, UK house prices increased by 3.1% in the 12 months to June 2013, up from a 2.9% increase in the 12 months to May 2013.

Predictably, vested interests like estate agents, surveyors and developers are crowing. The director of the Royal Institute of Chartered Surveyors, Peter Bolton King, claims the housing market is “on the road to recovery”.

I wish I could be so positive. But this “recovery” is not quite what it seems.

Here’s a lovely chart from the ONS report:

No, you aren’t seeing things. That is indeed an 8.1% increase in house prices in London. Even the rest of the South East doesn’t run it close – though more on the South East’s supposed recovery shortly. So what on earth is going on in London?

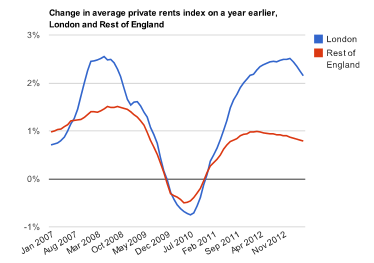

This might have something to do with it:

The Mayor of London’s property report (from which this graph is taken) says that “average private sector rents in London are around twice the national average”. But mortgage interest rates have fallen, at least partly due to Government intervention. Consequently, buy-to-let purchases are increasing at a rate of knots as existing and would-be landlords jump on what looks like a gravy train. Across the country, the Council for Mortgage Lenders says that buy-to-let mortgages have increased by 19% in volume and 31% in value in the last year. Much of that increase has happened in London. Although….BBC Newsnight, in its special report on buy-to-let as an alternative investment for disgruntled savers getting rubbish returns on their deposits, focused on Southend. The South East’s 2.9% increase is also partly due to increasing buy-to-let lending, it seeems.

But buy-to-let is not the only – or even the principal – cause of booming house prices in London. According to one estate agent surveyed by This is Money, 85% of prime property sales in London are to foreigners. And a report by the FT in July 2013 said that a record 82% of property sales were to overseas residents. Not immigrants – but people who live overseas and have no intention of moving to the UK. Many of these houses are bought simply as investments and remain empty once purchased.

So there is actually very little recovery in the London residential housing market. The 8.1% increase in house prices is due to inflows of hot money from overseas residents looking for safe investments (helped by the relative weakness of sterling), and a booming buy-to-let market due to high rents.

But what about the rest of the country? Well, there seems to be something of a North-South divide. Apart from London, house prices in the South East, West Midlands, Wales and the East are all growing at 2-3%. But elsewhere they are stagnant or falling.

As I noted above, it appears that buy-to-let has something to do with the rising prices in the South East. And it may also be influencing price rises in other regions too. However, it does appear that the Government’s schemes to encourage first-time buyers are working. This chart shows the rate of increase of house prices by type of buyer. The evident spike at the beginning of April 2013 coincides with the extension of the Help to Buy mortgage deposit guarantee scheme to existing properties as well as new builds. There is little doubt that this enabled first-time buyers to borrow more and therefore buy more expensive property.

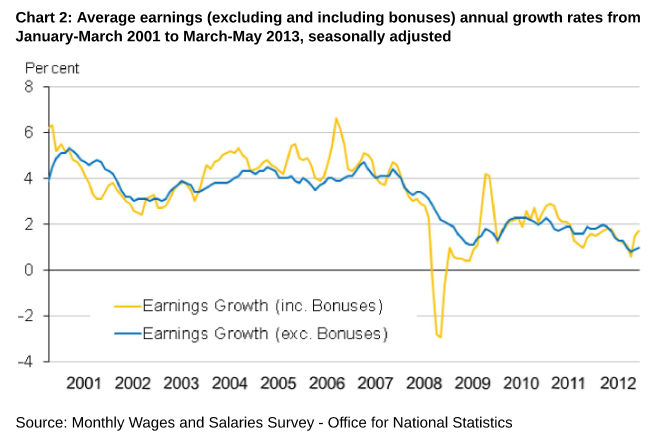

Would someone please explain to me why it is such a great idea for the Government to encourage first-time buyers to take on bigger mortgages at higher loan-to-value at a time when interest rates are at unprecedentedly low levels? The current low mortgage rates are by no means fixed in stone: Funding for Lending has reduced rates for borrowers, but there is no guarantee that they will remain low. Has no-one learned from the American housing crash of 2007, in which people with adjustable-rate mortgages suddenly found that the rate adjusted by far more than they could afford, and were forced into default? Where are the wage increases that support this increase in debt? This chart from the ONS shows that the rate of growth of wages is well below CPI, currently 2.8%, so real wages are actually falling:

I can’t see how such expansion of lending, and the resulting rise in house prices, is remotely sustainable. The economy is not growing, real wages are falling and living costs are rising. I really don’t buy the argument that rising house prices will somehow bootstrap the entire economy into sustainable growth. I’m in agreement with Moneyweek’s editor-in-chief, Merryn Somerset Webb. Speaking to the BBC, she said:

“I tend to think rising house prices are terrible news. It’s an entirely unproductive part of the economy,”

To my mind, unless economic activity increases and real wages start to rise, the housing market is bound to crash in due course, and the banks with it. Such rises in house prices are simply not sustainable in a flat economy with falling real wages. Encouraging house price rises under such circumstances is unbelievably stupid economic policy. But then this isn’t about economics, really.

The supposed “housing recovery” is due to three things:

- purchases of prime real estate in London by foreigners who have no intention of living in the UK but are attracted by the weakness of sterling

- expansion of the buy-to-let market by investors desperate to find some yield in a very low interest rate environment

- Government schemes to encourage people to buy houses on the assumption that interest rates will remain low for a long time to come.

Really it is entirely illusory. It has been deliberately engineered by a Chancellor whose sole aim is to ensure outright victory for his party in the 2015 general election. By pushing up house prices, he ensures the support of his core vote: by encouraging people to buy and sell property, even at unsustainable prices, he hopes he can can claim to be the Chancellor who “got the economy moving”. No wonder the loud complaints from savers (many of whom are Conservative voters) about low interest rates appear to be falling on deaf ears. No wonder Carney (with the tacit approval of the Chancellor) issued “forward guidance” that interest rates will remain on the floor until 2016. Markets were beginning to price in rate rises, but no way can rates be allowed to rise until after the 2015 election. The Conservative party’s victory depends on it.

As my regular readers know, I am determinedly politically non-aligned, so what I am going to say now will probably shock a lot of people. Osborne’s behaviour both angers and frightens me. He is playing brinkmanship with the UK economy to achieve political ends. Nothing he does makes much sense from an economic point of view – which is why the flagship Help to Buy scheme has been universally panned, even by his own department and by people from his own party. But if you view his actions as entirely determined by his desire to secure a Conservative victory in 2015, it all makes perfect sense. He is dangerous.

Related links:

House price inflation continues to rise, says ONS – BBC News

UK House Price Index, June 2013 – ONS (pdf)

UK Consumer Price Inflation, June 2013 – ONS

London Housing Market Report – Greater London Authority

Buy-to-let lending tops £5bn in second quarter – CML

London for Sale! – This Is Money

Foreign investors behind record 82% of London property activity – FT (paywall)

Funding for Lending Scheme – Bank of England

Help to Buy Scheme – HM Government

Help to Buy Scheme: how it works – Guardian

Funding for Lending scheme viewed as mixed success – FT (paywall)

BBC Newsnight Friday 09/08/13 (video)

Comments are closed.