Global Manufacturing Steadies as She Goes, or Does She?

By Edward Hugh

This post first appeared on my Roubini Global EconoMonitor Blog “Don’t Shoot The Messenger“.

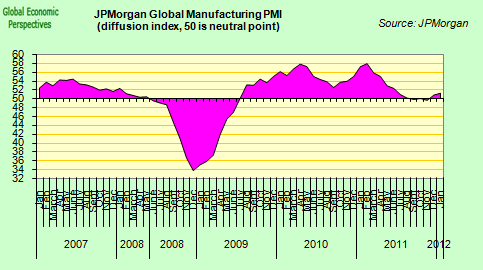

The year got off on a much better foot than might have been expected, at least as far as global manufacturing is concerned. As the JP Morgan report puts it:

“The global manufacturing sector continued to record below trend growth at the start of 2012. At 51.2 in January, the JPMorgan Global Manufacturing PMI™ rose to a seven month high, but remained below its long-run average (51.8). Manufacturing output expanded for the second successive month in January, as new orders rose for the first time since last August”.

“The cyclically sensitive new orders-to-inventory ratio also moved higher, reaching a ten-month peak. Although rates of expansion for both output and new orders were the fastest since last June, they were still only modest at best. Growth of production was recorded in the US, Japan, Germany, the UK, India, Eastern-Europe, the Netherlands, Austria, Canada, Switzerland, Turkey, Brazil, South Africa and Denmark”.

“International trade volumes improved for the first time in six months during January. Growth of new export orders was led by India, the US and Turkey. China, Japan and the UK all reported modest increases, in contrast to the declines seen in the Eurozone, Russia, Canada, South Korea, Taiwan and Brazil”.

So the fall in global manufacturing has flattened out, even though the bounce back has more of a dead cat look about it than anything else. As usual in recent months the report was very much a mixed bag.

Core vs Periphery Monotony?

Euro Area results were divided between the core countries which moved timidly back towards expansion, and those on the periphery where conditions were simply less recessionary than they had been at the end of last year.

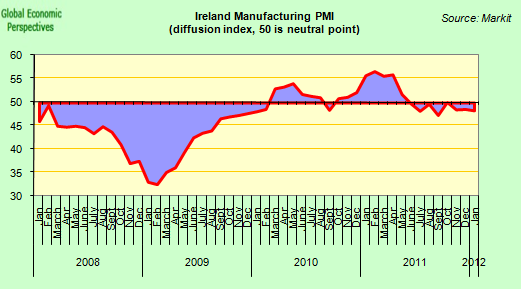

Surprisingly both Greece and Ireland bucked the trend and deteriorated, with the contraction in Greek output setting another series record for the country. Personally I have long held-and-expressed doubts that the people responsible for administering the Greek programme (namely the Troika) knew what they were doing, but I now find it hard to see how anyone else can still seriously maintain that they do. Avoiding Euro collapse, and total financial Armageddon and all those horrid things are most worthy objectives, but I think the Greeks will simply have to learn to live with an economy whose back has been broken, and where possibilities of things getting back to normal are slim. Someone said to me this morning, but “time cures, doesn’t it Edward?” Unfortunately I think the responsible answer is that this time it won’t.

Then again, the Greek situation is not news to the Troika who have long claimed their programme wasn’t working because the Greeks weren’t cooperating, but the Irish result might have thrown a rather larger bucket of cold water over their hopes, since it suggests that despite all those optimistic pronouncements the country is a long way from being out of the woods.

In his comment on the Irish Manufacturing PMI survey data, Brian Devine, economist at NCB Stockbrokers said:

“The first NCB PMI of 2012 has got a familiar feel to it; domestic demand continues to drag and export orders continue to expand. The headline composite index contracted for the third month running (48.3 from 48.6), with output contracting more sharply than last month (47.3 from 48.7). New orders overall continued to contract (46.8), but export orders expanded once again (50.9). 2012 is going to be the fifth year in a row in which domestic demand will contract and if GDP is to expand, Ireland will need an improvement in the euro area economy in H2 2012.”

And I think this is the whole point all along the periphery, the excessive debt overhang makes their economies almost entirely export dependent, yet after years of credit-driven consumption-abuse their economies are totally distorted and their manufacturing industries are just not big enough to do the work. Ireland`s industrial base is in better shape than many, but even in this case expanding exports coupled with falling domestic demand simply means the economy flatlines. Ireland’s central bank now expects GDP to grow just 0.5% this year, while the fiscal deficit target is still a hefty 8.6% of GDP, so not much in the way of “bang for the buck” there. The country’s debt will now surely peak above the 118% currently anticipated by the IMF due to the lower growth expectation, and it is hard to see the country achieving debt sustainability without the kind of debt assistance being given to Greece, and which markets increasingly expect will be offered to Portugal.

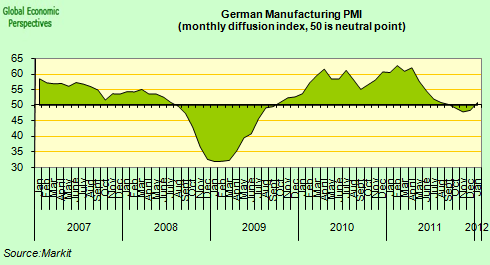

Germany Not As Strong As It Might Be

Even the German manufacturing report gave reason to be cautious. The index reading was mainly up because the current output component was up, and this component was up because backlogs of work were reduced at a faster rate despite the fact that incoming new orders declined. And why did manufacturers reduce backlogs more quickly despite falling orders? Because they feel that the debt crisis has turned the corner, and that things will now improve. Despite the evident positive contribution made by the ECB 3yr LTRO they may well still be in for a rude awakening.

As the report says:

“The increase in the headline index was primarily driven by a robust rebound in output growth at the start of 2012. Production levels rose for the first time in four months and at the fastest pace since June 2011, led by an upturn in both intermediate and investment goods output. Higher output volumes were supported in part by greater work on unfinished business in the manufacturing sector. This was highlighted by backlogs of work falling in January for the fifth month in a row”.

“Meanwhile, new orders continued to decline at the start of the year, although the rate of contraction was relatively modest and the slowest in the current seven-month period of reduction. Latest data indicated that the decline was driven by a marked fall in new work received in the consumer goods sector”.

“A further solid drop in export sales contributed to the overall fall in new business levels in January. Lower levels of new work from abroad have been seen in each of the past seven months, largely reflecting weaker global demand and uncertainty about the economic outlook. In line with recent trends, lower new export orders were recorded across all three market groups monitored by the survey”.

And as Chris Williamson, Chief Economist at Markit puts it in his general Eurozone comment:

“Anecdotal evidence from survey respondents indicates that much of the improvement appears to be based on business and consumer confidence reviving, in the belief that the worst of the region’s debt problems are behind us and that a new credit squeeze may be averted. As such, the outlook remains very much dependent upon further progress in resolving the crisis.”

Chris Williamson is absolutely right. The situation is extraordinarily fragile, and much depends on how the Euro debt crisis evolves. The ECB’s 3 year LTRO has stuck a finger in the dike for the time being, but without more decisive moves to reform the Euro Area’s institutional architecture for how long will it last?

Booming EMs

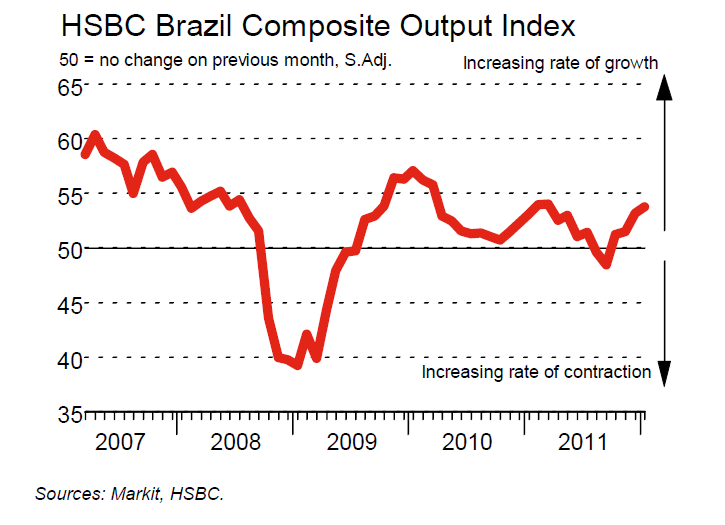

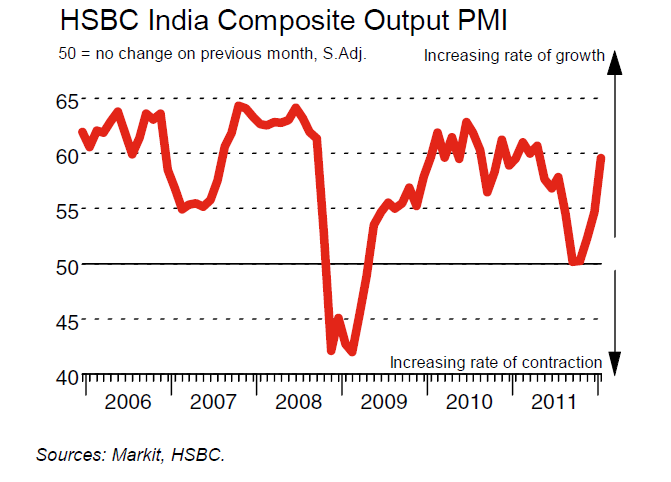

Among emerging markets the situation is very different, and Brazil and India are now both showing real signs of recovery. The recovery in manufacturing is significant, but the composite indexes (which cover both services and manufacturing) show a really strong surge in activity.

Curiously, only this week the Colombian central bank started intervening in the currency markets again, buying dollars in an attempt to stem the rise in the peso which is starting to crimp export competitiveness.

Emerging market nations such as Colombia have faced a flood of cheap money in recent months as near-zero interest rates in developed markets prompt investors to seek higher yields, pushing up their currencies and strengthening their economies. The peso has firmed almost 7 percent this year, making it one of the best performing currencies among the world’s 36 most-traded, partly thanks to strong foreign direct investment inflows. The dollar purchase program, which previously ran through September 2011, would re-start on Monday, the bank said in a statement.

The Euro As A Global Funding Currency?

So as core European banks ramp up their deposits at the ECB, and credit conditions on the periphery continue to worsen, a lot of the extra liquidity being generated either at the ECB or the Fed is simply seeping out and fueling demand in emerging markets, which is a plus for exports, as long as your manufacturing industry is big enough and competitive enough for this to matter. As I say, much of the European periphery is facing an outright credit crunch as banks tighten their credit standards. The FT’s John Dizard put it this way:

There was a lot of earnest chitchat last week about the ECB’s Euro Area Bank Lending Survey, which reported a tightening of lending standards and a decline in the demand for credit. The results, in the bureaucratic tradition of false precision, were reported to accuracies of one percentage point. So, for example, the report tells you that credit conditions were tightened on 42 per cent of long-term loans in the last quarter of 2011, compared to 20 per cent in the preceding quarter.

What the ECB’s survey did not tell you was what is meant by “tightening”, and exactly where in the euro area this undefined tightening occurred, and, where it did not occur. Let me put it this way: if you are a German machinery exporter, your bank just cut the cost of your receivables financing. If you are a Spanish commodities trader or Italian aircraft lessor who had a line of dollar credit from a French bank, you are probably out of luck.

In an article entitled “ECB ‘saves’ banks as economies sink” Edward Chancellor makes similar points:

Over the past couple of months, the cost of Italian two-year debt has fallen from 7 per cent to around 3 per cent. As investors’ fears abated, the share prices of European banks rebounded. The vicious cycle that gripped Europe’s financial system appears to have ground to a halt.

Unlimited access to ECB money means Europe’s banks will have cash on hand to repay any loans that become due this year. Since deposit outflows can quickly be replaced with ECB funds, the periphery is less vulnerable to bank runs. Now that the liability side of their balance sheets has stabilised, European banks will not be in such a rush to dispose of assets.

At around 1 per cent, LTRO money is also very cheap. Barclays estimates that lower funding costs will boost the earnings of eurozone banks by 4 per cent. Clever bankers may do even better – Italy’s Unicredit, for instance, is using money from the ECB to repurchase its own hybrid bonds at a large discount. Increased profits reduce the amount of equity capital that the banks will need to raise. More stable share prices diminish the risk of dilution for bank shareholders.

Mr Draghi’s largesse, however, cannot cure all of Europe’s woes. Within the eurozone, banks have becomes increasingly reluctant to lend across borders. Banks in the core of Europe are reportedly still looking to reduce exposure to the more spendthrift members of the currency union. On its own the LTRO is unlikely to reverse this financial Balkanisation. European banks remain massively leveraged. They will continue to shrink their balance sheets, albeit at a more measured pace.

Nor can a wave of Mr Draghi’s monetary wand remove the eurozone’s macroeconomic imbalances. Much of the periphery remains uncompetitive relative to Germany.

The latest Euro Area Bank Lending Survey reports that 35 per cent of banks tightened lending conditions to European non-financial corporations. The money supply in the periphery contracted by 4 per cent in the year to November. Spanish industrial production fell by 7 per cent over the same period. The dire economic prospects for the periphery are exacerbated by Germany’s insistence on fiscal austerity.

The ECB’s action has brought a liquidity crisis to an end. But it is unlikely to spur lending in the real economy. Until the economies of Europe’s periphery start to grow, concerns about their solvency will continue.

So what is happening? Well the massive liquidity easing engaged in by the Federal Reserve in the US and the Wall of Money sent out by the ECB has loosened credit conditions, but not in the intended economies. We have been here before during QE1 and QE2, but if you look at the first chart in this blog (the global manufacturing one) you will see that we are hardly getting a “mountain” of growth, indeed at this moment what we have is little more than a bump in the road (on aggregate).

Confidence is back globally, as fears of an imminent Euro unwind recede, and “risk” is “on again”. Cheap liquidity available for tapping in over-indebted developed economies is flowing into rapidly growing emerging markets again, risking yet more distortions in their developing economies. One sign of this is the Colombian attempt to stem the rise in the peso which would further crimp export competitiveness. In general “carry is king” once more, and the Euro has even become the funding currency of reference. To cite William Kemble-Diaz in the WSJ:

Canny foreign-exchange investors are increasingly tempted to borrow euros to fund bets in higher-yielding currencies, even though it is a lot cheaper to borrow dollars.

The combination of low European Central Bank interest rates that are likely to fall further, and growing confidence that the euro is set for a big slide this year, lines the currency up as a good bet to sell in search of juicier bets elsewhere. In the market’s parlance, that makes it a funding currency, equivalent to nailing a “for sale” sign on its fence.

It is an unusual role for the common currency, and one normally grabbed by the dollar and yen. While low, ECB interest rates at 1% are still four times higher than, say, the U.S. Federal Reserve’s, so when investors feel broadly confident the euro usually rises as traders are drawn to its higher returns. Now, though, a poor outlook for the currency’s value and quirks in the interbank borrowing market mean typical trading patterns are being turned on their head.

The three-month euro-dollar basis swap, which is a function of spot and forward foreign-exchange prices and prevailing interest rates as well as a bellwether for dollar funding stress, has improved to minus 86 basis points from as low as minus 165 basis points in late November, when worries about “another Lehman” filled the air.But that figure remains deep in the red when, if all were well, it would be closer to zero. For market participants seeking a funding currency, that, combined with the euro’s weak outlook and slowing euro-zone economy, makes for an increasingly tantalizing combination.

(See Bloomberg’s Masaki Kondo and Hiroko Komiya on the same topic here).

China The Odd Man Out?

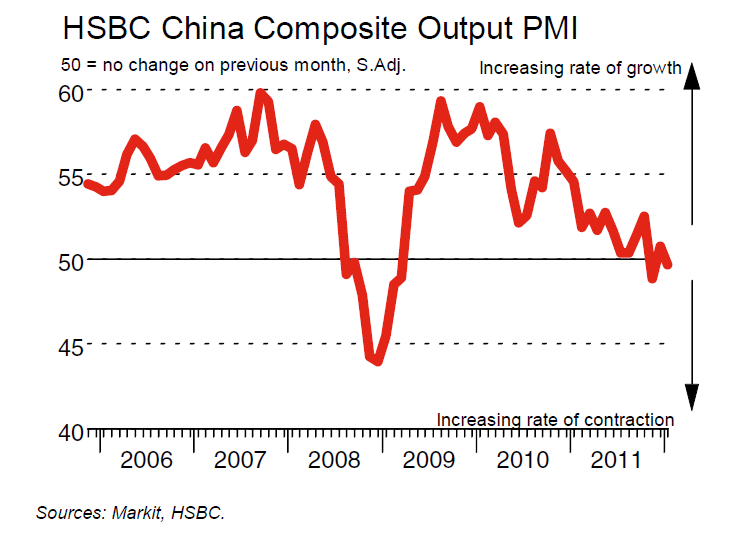

But even here we find yet another anomaly. While many emerging markets are beginning to boom, China (oddly) failed to spring back,. This suggests the country may really be feeling the housing slowdown/bust pinch.

This is a possibility that Global Insight’s Alistair Thornton definitely entertains.

In combination with better-than-expected numbers out of the United States and what would appear to be an improving situation in Europe, a relatively mild slowdown in China would prove a boon for global markets. Unfortunately, the situation is not entirely positive, despite some signs of resilience in China’s deceleration. IHS Global Insight has picked out a few “behind-the-scenes” indicators which give a slightly different take on the macro climate.

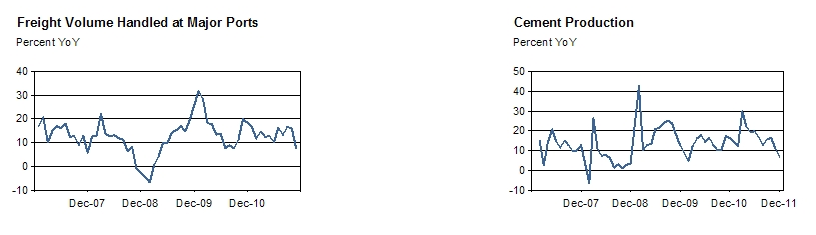

While it is important to note that micro indicators do not necessarily have macro implications, they can help shed light on nascent trends, particularly when there is a modicum of scepticism about the quality of Chinese data. Taking a cue from Vice-Premier Li Keqiang, who when Party Secretary of Liaoning joked that China’s provincial GDP figures were “man-made”, we first turn to freight volumes at major coastal ports. China’s export growth has been suffering under the weight of unravelling demand in advanced economies, and growth in freight volume sagged considerably in November—down to 8% y/y from October’s 16%. This suggests lacklustre demand both overseas and, to some extent, in China, which will drag on growth going forward.

To give him an indication of the state of domestic activity, Alistair took a look at cement production widely regarded as a key feeder for the nation’s property sector, which itself is a key component for investment and the wider economy. What he found was that cement production growth slid to 7% y/y in December (see chart above), down from 11% in November and 17% in October. T

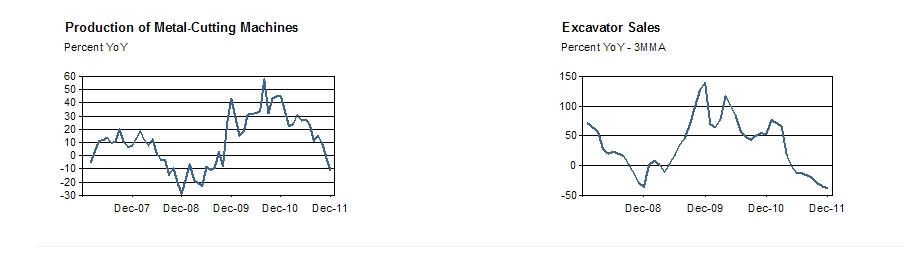

This also fits in with data showing a recent contraction in real-estate construction and anecdotal evidence suggesting an extremely weak project pipeline. More worrying, he found that machine production and machinery sales indicate a severe contraction in construction activity to come.

While metal-cutting machines sound an obscure piece of kit, they are an integral part of China’s construction and investment economy. They are highly pro-cyclical, with the global downturn of 2008–09 pulling production growth to around -30% y/y, before ultra-loose credit policy and construction activity buoyed growth to over 50% in 2010. As of November, however, y/y production growth has been negative, with December’s figures sinking to -11%.

While this demonstrates receding construction activity, the pull-back in machine production has not yet reached the nadir seen in 2008–09. Sales of excavators, on the other hand, have fallen below those depths, reflecting the intense pressure stacked on the real-estate sector. With data from China Construction Machinery Business Online, smoothed using a three-month moving average, we can see that sales growth contracted almost 40% y/y in December.

Little Momentum In Non-Europe Developed Economies

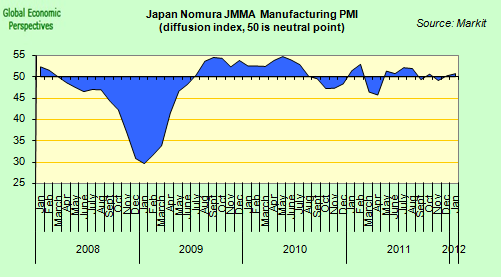

Moving back to the developed world, Japan showed marginal growth, but far from sufficient to help the country overcome the growing sovereign debt problems. The strong yen and the weaker demand from both Europe and China is clearly taking its toll, despite many earlier predictions of a “V shaped” bounce back.

As Alex Hamilton, economist at Markit and author of the report said in his comment:

“January PMI data suggest that the sector has begun 2012 on a firmer footing following a year in which supply chain disruptions emanating from March’s earthquake and flooding in Thailand disrupted firms’ production plans. However, the survey findings paint a relatively flat growth picture, and demand for Japanese manufactured goods remains muted. Although new business and new export orders both returned to growth in January, rates of expansion were marginal. Companies cited sluggish demand from China and Europe as the principal drag on new export order growth. Some respondents also mentioned persistent yen strength, which made the cost of imported items relatively cheaper and by doing so contributed to an easing in the pace of input price inflation to a 15-month low.”

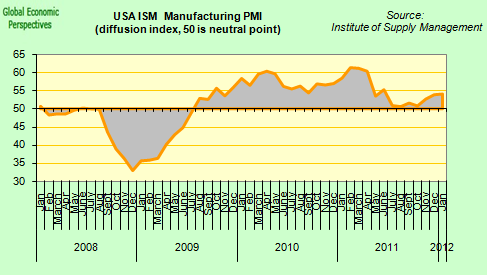

And finally, even while the US manufacturing sector continued to grow in January, the momentum behind the expansion remained far weaker than in earlier post-recession activity bursts. Hence the substantial fiscal deficit plus the promise of keeping interest rates near zero till at least the end of 2014 are still having a hard time producing output growth, with the implication that the Economic Cycle Research Institute US Recession call may not turn out to be as “loony” as many appear to think it is.

Comments are closed.