The Massendowngrade Effect

By Edward Hugh

This post first appeared on my Roubini Global EconoMonitor Blog “Don’t Shoot The Messenger“.

Well, that was the week that was, wasn’t it? It started with a cheerful, upbeat market response to both the impact of the ECB’s 3 year LTRO and the growing impression that Hungary was going to make some sort of “one-off” deal with the IMF, and ended near the depths of despair as S&P’s announced the downgrade of 9 Euro Area countries, while the EU Commission worked hard to reinforce the impression that it was about to launch legal proceedings that could even lead to the temporary suspension of Hungary from the EU. It was a time of bitter sweet experiences, which started with Tamás Fellegi (that’s him smiling in the photo below) heading off for his scheduled interview with Christine Lagarde. Then we learnt that the German economy had grown by a brisk 3% in 2011, only to have our hopes dashed by the clarification that most of the growth was in the first 9 months of the year, and in fact the country probably entered recession in the last quarter.

Just as we were recovering from that initial shock, Irish stockbrokers Goodbody poured even more cold water on our breakfast cornflakes by telling us that Ireland would probably need a second bailout, since economic performance in 2012 was likely to be below expectations, while prevailing financial conditions would make an early return to the financial markets virtually impossible. Our spirits were fleetingly brightened by the news that Spain had managed a successful bond auction, but the cork was just as swiftly rammed back into the bubbly bottle as it had been pulled out when we discovered that Italy had not, and that LCH Clearnet had promptly reacted by raising the margins on the country’s debt when posted as collateral.

On the other hand Thursday did give us another brief soothing interlude, as Mario Draghi reminded us of all the beneficial consequences of the recent 3 year LTRO (Long Term Repo Operation), and cheered our spirits by informing us that he was not lowering interest rates again at this stage due to the growing signs of stabilisation his technical staff had been able to identify. “According to some recent survey indicators, there are tentative signs of stabilization of economic activity at low levels,” he told the assembled journalists, although he did go on to warn that the debt crisis continued to pose “substantial downside risks” to the economic outlook and the ECB stood “ready to act” if need be.

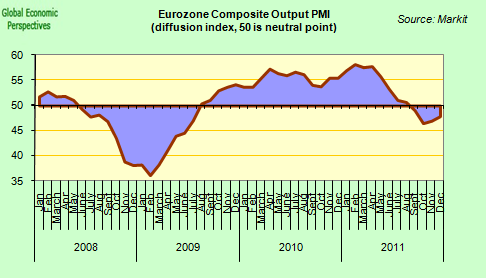

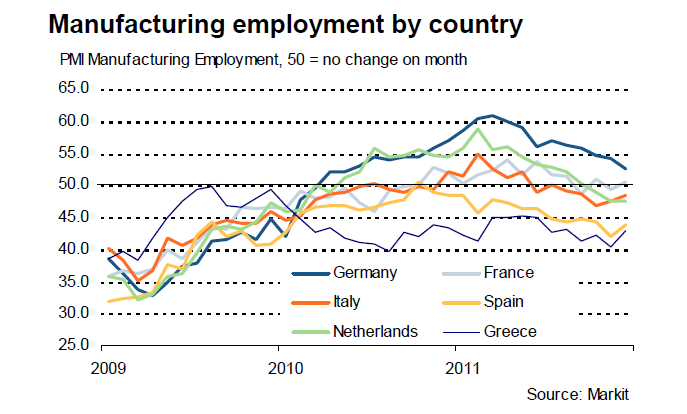

Apart from the evidently weakening inflation, possibly the most important single indicator he will have had in mind in making the above statement would be the monthly PMI survey. The composite index (which combines manufacturing and services) shows economic activity continued to contract in December, but at a rather slower rate than in November, and in fact the rate of contraction in November was slower than the one recorded in October. So things are getting worse more slowly!

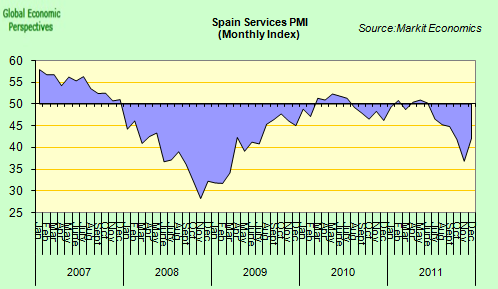

Despite the evident differences between countries in their rate of deterioration, the stabilisation pattern is pretty generally reproduced across the Euro Area. In Spain, for example, where services activity plummeted in November (at rates reminiscent of the last recession), the decline was significantly slower in December, although it was still, of course, a substantial decline.

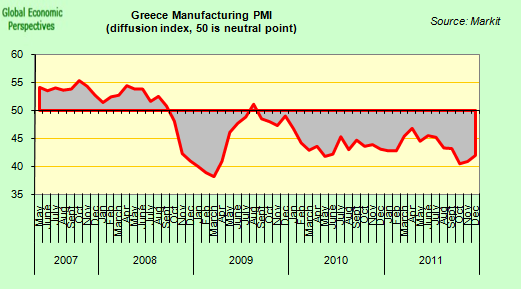

Even Greece’s war-torn manufacturing sector showed signs of “contraction weariness” in December, although I fear that had the contraction continued at its earlier breathtaking pace we would soon have little left.

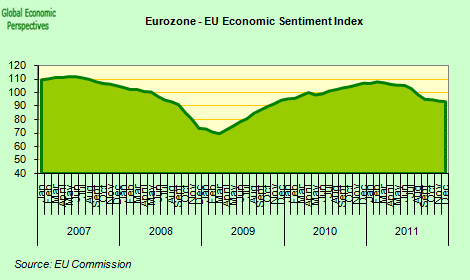

The EU sentiment index has also fallen much more slowly in the last two months, indicating that confidence is not deteriorating as rapidly as it was.

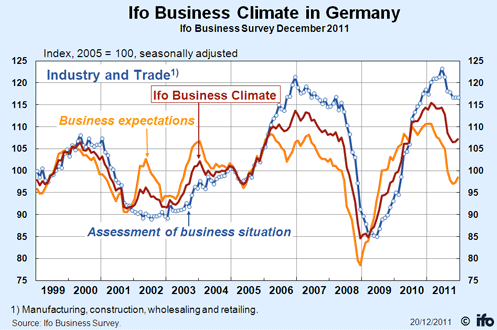

And the widely followed German IFO Business Climate index has perked up slightly in the last couple of months.

So Mario Draghi is absolutely right, stabilisation is precisely what we see. But this is stabilisation during a decline, and there is little in these indicators to tell us which way the next move will be, and in fact the few forward looking components we have suggested things might be about to get worse rather than better, a point which was not lost on Markit’s Chief Economist, Chris Williamson, who said in his comment accompanying the monthly PMI report:

“The uplift in the Eurozone PMI in December does little to dispel fears of the region sliding back into recession. Despite the upturn, the fourth quarter saw the steepest contraction since the spring of 2009, and forward-looking indicators suggest that a further decline is on the cards for the first quarter of 2012. In particular, orders for goods and services continued to collapse, suggesting that output and employment will be cut as we move into the new year”.

Of course, as everyone is by now only too well aware, the week finished on a crescendo as S&P’s announced the widely anticipated downgrade of nine Euro Area countries. That being said, surely pride of place in this agitated week must belong to Hungary, whose bleary eyed Prime Minister Viktor Orban can be seen in the photo below. It is early morning, and he probably hadn’t slept that well after learning that the IMF would defer to the EU on all matters relating to whether his country was in compliance with its Treaty obligations before taking any decisions on future loans.

As one country after another temporarily surrenders its right to an elected government to put itself in the hands of the technocrats (as Hungary did in 2009, before the election of the Orban government) I cannot help asking myself whether recent developments are mainly the result of the countries peculiar (and almost unique) history, or whether it is giving us an idea of the sort of thing we can expect to see if simple austerity as it is being practised all along Europe’s periphery doesn’t work out as planned. Certainly Mario Monti is alive to this possibility, as he said in an interview with Die Welt Online this week (German only I’m afraid), unless Europe’s policy is flexibilized it will be a case of “after me the populists”.

All Alive And Well On ECB Cool Aid?

Perhaps the main point to take to heart from the events of the last week is the way the recent ECB liquidity measures have apparently been able to stabilise the debt crisis, at least for the time being, even while it is not clear that they will have the same success stabilising the deterioration in the respective real economies.

In a liquidity-providing operation which some have described as “unleashing a wall of money“, in the week before Christmas more than 500 EU banks borrowed a total of €489 billion in three-year loans – equivalent to roughly 5 per cent of eurozone gross domestic product and the largest amount ever provided in a single ECB liquidity operation. In fact only about €190 billion of this was new money, since the majority of the borrowing involved the consolidation of lending that had already been taking place on a shorter term basis.

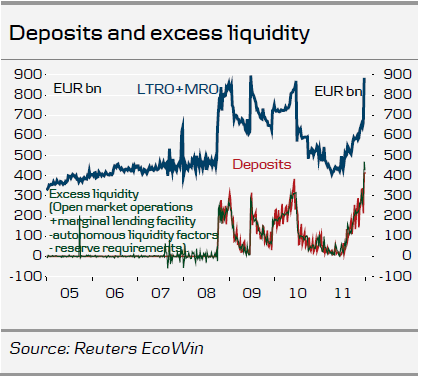

Despite the size of the demand, and some relatively successful bond auctions, much attention is still focusing on the way Eurozone banks’ overnight deposits with the European Central Bank have been rising in the wake of the move. In fact these themselves hit yet another all-time high last Thursday according to the ECB, with the quantity deposited hitting €489.906 billion, up from €470.632 billion the day before. This phenomenon has lead some analysts to suggest the operation may be a failure. Such a judgement would be a premature and erroneous in my humble opinion.

It’s The Real Economy, Stupid!

In order to assess the extent to which the recent ECB measures have succeeded we need to think about what the objectives really were. In the first place the bank clearly hoped the commercial banks would use some of the money borrowed to buy new issue government bonds in the primary market, and earn themselves a bit of “carry” (the difference between what it costs them to borrow from the central bank and what the bonds purchased pay) in the process. The much needed additional income will help them improve their bottom lines and allow them to accumulate some additional capital to help with their capital ratios. This has lead some observers, like Nomura’s Kevin Gaynor, to argue that the ECB is now doing overt (as opposed to covert) QE. In some senses this is surely the case, since the bank was already doing what some called QE by stealth way all the way back in 2009 (as Claus Vistesen argued here, and I argued here).

But before digging into all this a bit further, let’s go back to the issue of those growing overnight ECB deposits. For some observers the very size of these deposits constitutes evidence that the ECB 3 year LTRO isn’t working as anticipated.

This argument, as Danske Bank’s Senior Economist Frank Hansen argues, is misleading, since the volume of ECB deposits only give us a measure of aggregate excess liquidity across the Eurosystem, and doesn’t tell us anything about the distribution of that liquidity between countries or between banks.

“Does this mean that the operation has failed to stimulate government bond purchases? No, not really. If a bank uses money from the LTRO to buy government bonds (or any other paper) in the secondary market, the amount will still show up as a deposit at the ECB (now on behalf of the seller’s bank). If a bank buys government bonds in the primary market, the amount will also show up as bank deposits at the ECB if the government spends the receipts or places them at a private bank. Thus, the increase in deposits does not imply that the 36 months LTRO has failed to stimulate government bond purchases (or other trading for that matter)”.

So basically, if we think for a moment about maturing, and not new, additional issue, government bonds, then commercial banks along the periphery buying the replacement issue can allow their peers in the core to recover their investment, and park the money. The only way the money from these sort of bond transactions doesn’t show up as excess liquidity is if the national government concerned places the takings on deposit at the central bank, or if an investor takes the money they have recovered from a redemption out of the Eurosystem. The same goes for private bank debt, which often just moves from being a liability one bank has with another commercial bank in the Eurosystem to being a liability with the ECB. Naturally the bank that recovers its money may well then park the proceeds on deposit and hence it will show up as excess liquidity at the ECB.

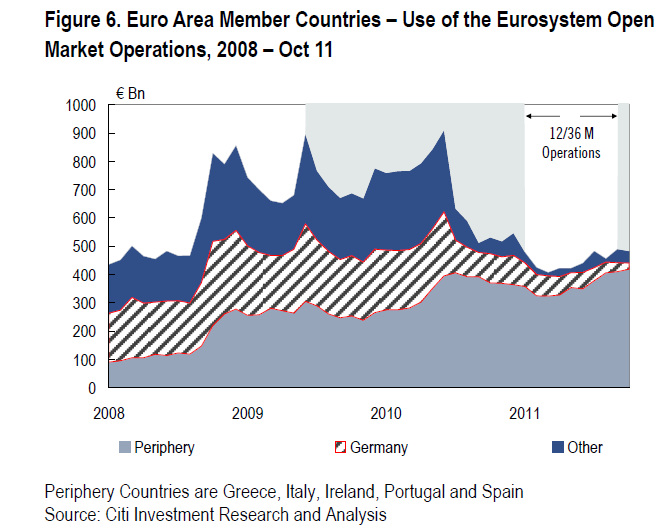

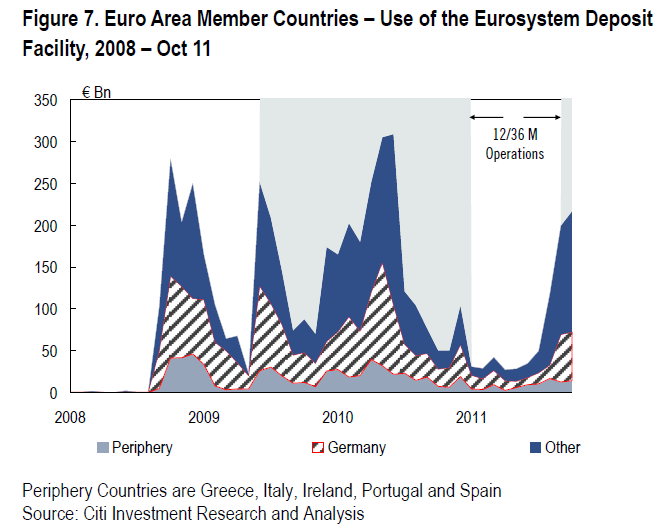

So, while short term liquidity needs may be being catered for (at least up to 3 years), there may be a deeper phenomenon at work via the LTRO, whereby the core leaves the periphery. In fact that seems to be happening. The charts below (which were prepared by Citi Research) show the situation up to the end of October (latest data), and make clear that it is commercial banks on the periphery who are, in the main, making increased use of the ECB’s open market operations, while it is banks in core Europe who are using the deposit facility.

There is no reason to suppose that data post October will reveal any fundamental shift in tendency. Spanish banks, for example, increased their ECB borrowing from roughly €70 billion in September to €118 billion in December (nearly a €50 billion – or 75% – increase), while use of the deposit facility only went up from €9 billion to 15 billion, so the Spanish banking system clearly needs this liquidity.

Write-downs On The Liabilities Side?

Another area where the transfer of liquidity doesn’t show up as a change in aggregate excess liquidity is when banks offload their wholesale liabilities to other Euro Area banks and refund via the ECB. Here again, if they do it smartly, they can even earn a bit of “quasi carry” in the process, by buying back their debt at well below face value from those who are anxious to exit the periphery, and then refinancing at the ECB without writing down the underlying asset. This could be termed a liability “write down”, and again the procedure earns the bank a nice bit of income which can subsequently be used to help the recapitalisation process.

Take the Portuguese Bank BPI (the country’s fourth largest), which is making public tender offers to buy back its debt. If all concerned tender their bonds to BPI, BPI will pay something short of €1.5bn cash to investors. Mortgages which were previously sitting in one of their SPVs will return to their balance sheet, and ECB money will now be on the other side financing them allowing significant profits (and capital) to be reported. In this particular tender the smallest discount is 35% and the largest is 65%. Investors may initially baulk at the offer, since they will nurse a heavy loss (equal, naturally, to BPI´s profit) but ultimately they will probably be only too happy to be able to walk away from Portugal, and with some cash in their pocket to boot.

Iberian banks were already aware of the benefits of this kind of restructuring during the 2009-2010 liquidity wave, and went about quietly repurchasing their bonds (bank capital, securitizations, senior bonds) on a selective and private basis at a discount. Much of their reported profits in those years in fact came from either the ECB carry trade or this kind of transaction. So when we read that another Portuguese bank – Banco Espirito Santo – has just had €1 billion of debt guaranteed by the Portuguese state (a sovereign which can’t itself go to the markets) it isn’t hard to imagine that the process going on in the background is something similar to that seen in the BPI case, and that the debt is being guaranteed so it can go over to the ECB to be posted as collateral.

The National Bank of Greece has been doing something similar. They recently offered to buy back some €1.5 billion in covered bonds and preferred securities, offering 70% of face value for the covered bonds and 45% for the preferred hybrids. As the bank itself says, “The purpose of the offers is to generate core Tier 1 capital for the group and to strengthen the quality of its capital base….The offers would generate a gain for the group.”

And Italian banks would seem to be doing something similar, since they issued around €40 billion in government backed bonds specifically to take to the ECB. The bonds are held by the banks themselves and stay on their books to maturity, their only purpose being to provide collateral for use at the ECB. In fact Italian banks took something like €116 billion from the LTRO, or almost 25% of the total. Perhaps this is why Unicredit CEO Federico Ghizzoni and other European top bankers met ECB officials in Frankfurt back in November, to discuss new rules for collateral.

In Spain securitised mortgages sitting on the balance sheets of the bank-owned Fondos de Titulizacion de Activos could also be recycled in this way (here’s a complete list, although note that these Funds are regulated by Spain’s CNMV and not the Bank of Spain, which is why their presence is relatively unknown and people are able to accurately say that the central bank has been very strict on SIVs, since they weren’t their responsibility).

That something like this may be happening, with the ECB “buying into” public and private Euro Periphery debt while investors are discretely getting out is suggested by this report in Bloomberg:

The euro is losing the relationship with riskier assets that underpinned the currency in 2011 as the deepening sovereign debt crisis reduces the creditworthiness of even the biggest economies in the region. The 17-nation currency has fallen 8.7 percent against the dollar since October, while the Standard & Poor’s 500 Index has gained 3.4 percent, and the correlation between the two dropped to 58 percent from a record 91 percent in November, according to data compiled by Bloomberg. The euro had moved almost in lockstep with investments linked to growth, including stocks and the Australian dollar, since January 2011.

This decoupling is taking place as European Central Bank President Mario Draghi cuts interest rates and promises banks unlimited cash for three years to rein in soaring borrowing costs for governments… Strategists also anticipate more losses as the US economy improves while the euro zone shrinks, driving international investors away from the region’s assets.

So if the first two objectives were to help the struggling sovereigns, and enable the commercial banks to refinance their debt, then to some extent these objectives have been met. But what about the third objective, moving credit on the periphery to get the real economy moving again? Well, here the ECB’s measures are likely to have far less effect, and indeed what effect they do have may be in some way a mixed blessing, since the banks seem far more worried about demonstrating they have an adequate level of core capital than they are about participating in solutions to real economy problems.

Credit Crunch Is NOT Uniform

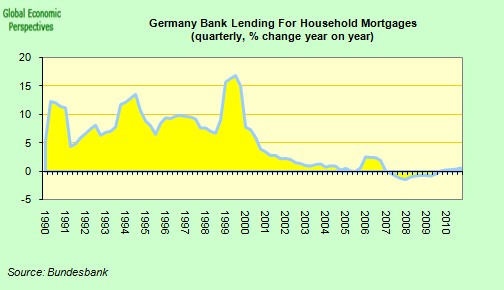

To understand why this simply increasing aggregate liquidity doesn’t necessarily help individual countries, it is important to realise that credit conditions in the Euro Area member countries are not uniform (a much more detailed exposition of this point can be found in this earlier post). In countries like Germany, Finland and the Netherlands, credit is more or less freely available, even if demand for it is limited – German corporates are awash with cash, and it has been a long, long time since German households were digging their way into debt.

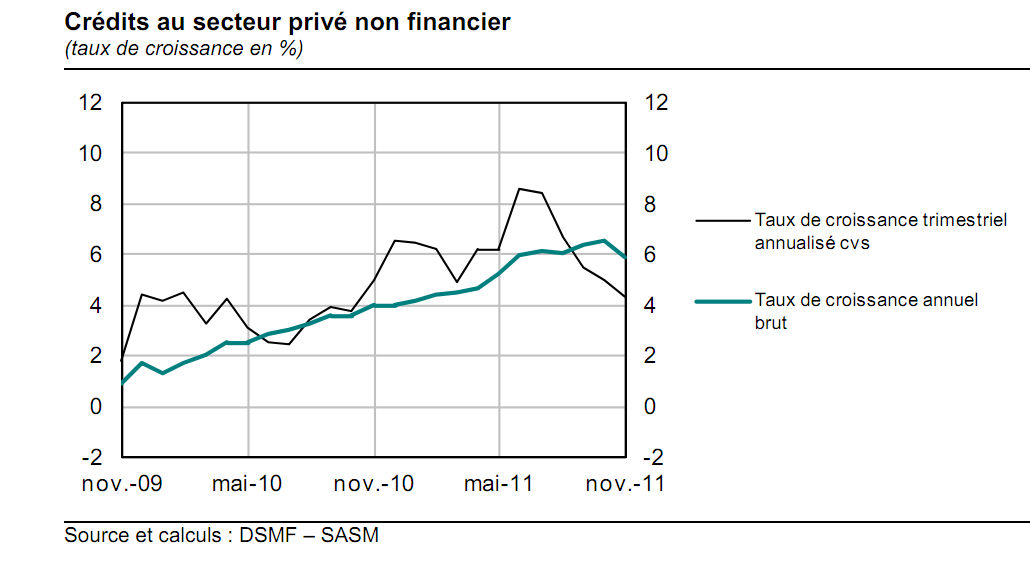

In France and Italy, banks are drawing in their horns, but credit is a long way from being frozen.

Although in France, the rate of new loan generation in the private sector has been sliding since mid summer, especially if you look at the thin black line in the chart below (Bank of France), which shows the rate of change on a three monthly rather than an annual basis.

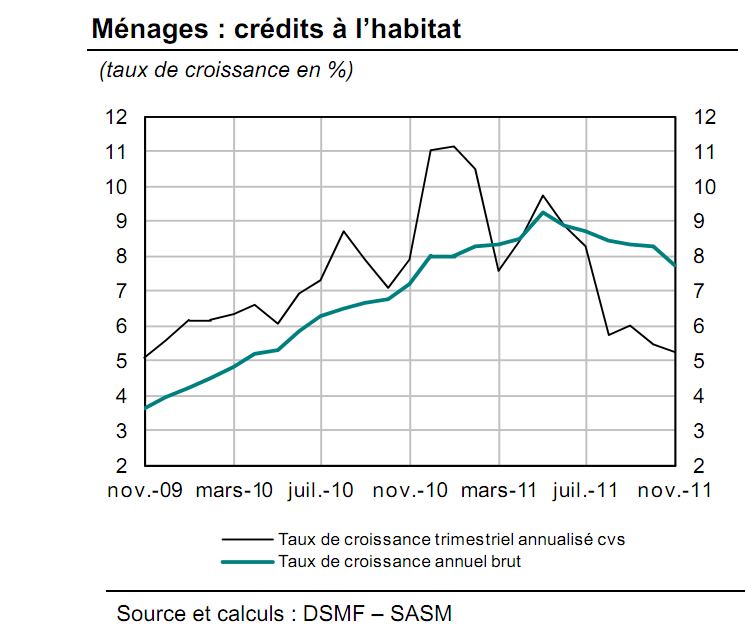

A similar position can be seen in the case of home mortgages.

Now in the French case, given that the private sector is not heavily overindebted, unemployment is not excessively high, and a demand for credit from solvent clients exists, it is quite possible that the ECB measures can help stabilise the situation, and put a brake on the implosion.

On the periphery, however, where populations are heavily indebted either directly, or via their sovereigns, where the economy isn’t functioning properly, and unemployment is high and rising, the problem isn’t only the unavailability of credit, but also the shortage of solvent clients who actually want to leverage themselves.

Day Of The Living Dead?

For increased liquidity to mean that credit becomes expansionary for the real economy again, it is the banks themselves who need to deleverage (and not simply write down their liability side), by disposing of the large volume of continually restructured but basically non-performing credit they have on their books. Behind the credit crunch in these countries lies a problem of massive economic structural distortion, produce by the lending and borrowing boom during the “good” years. What is needed is what Joseph Schumpeter referred to as a process of “creative destruction”, whereby some enterprises die so that others can be born, and naturally some loans are written off, despite the fact this has unpleasant effects on bank profitability and capital ratios. To really get credit moving again in some of these periphery economies, a large chunk of loans need to be written down, and support needs to be offered by the sovereign to enable this to occur.

Unfortunately the ECB’s liquidity provision could have precisely a perverse effect in this context, as it may well enable those who should die to stay alive. Commercial banks, at the discretion of their central bank, may now package straightforward bilateral commercial loans to present as collateral at the ECB. This measure, which in theory was intended to enable the banks to extend “good credit” may now enable them to restructure and keep on their balance sheet loans that should really be classified as “impaired” and somehow resolved.

In the case of Spain, for example, in addition to the properties they have acquired, banks still have outstanding loans of over €300 billion to developers on their books according to Bank of Spain data. The majority of these loans are not classified as either non-performing or sub-standard, and are hence considered to be “good” (I will refrain from saying “excellent”). In principle there is no reason why a significant number of these “good” loans cannot be packaged in some way or other to serve as collateral to be posted at the ECB. Naturally this takes some of the pressure off Economy Minister Luis de Guindos to establish a bad bank, since for the time being the ECB can, in part, serve this purpose for him. And if the banks write down their liability side a bit, then this may also help him with the €50 billion or so he estimates will be needed for bank recapitalisation. No wonder he feels the amount of public money needed will be minimal! The only real downside on this is that foreign investors may well be dumping Spain, while the country (which still runs a current account deficit) continues to have an external financing requirement.

None of this is either unequivocally good, or unequivocally bad, it depends. What the liquidity move will do is buy the banks time to sweat out some capital onto their balance sheets, and make them better able to withstand more of those dreaded “stress tests” (assuming, that is, that the European Banking Authority allows some “wiggle room” to enable them to keep maintaining their risky sovereign debt holdings). What it won’t do is help put the real economy straight, or allow the banks to get back to what some would consider is their basic task which is guaranteeing a normal supply of credit to the economy.

Working Against The Clock

All of which brings us nicely back to those horrid S&P downgrades. According to S&P’s own literature, the downgrades were prompted by a number of concerns:

Today’s rating actions are primarily driven by our assessment that the policy initiatives that have been taken by European policymakers in recent weeks may be insufficient to fully address ongoing systemic stresses in the eurozone. In our view, these stresses include: (1) tightening credit conditions, (2) an increase in risk premiums for a widening group of eurozone issuers, (3) a simultaneous attempt to delever by governments and households, (4) weakening economic growth prospects, and (5) an open and prolonged dispute among European policymakers over the proper approach to address challenges.

If we look at the list of 5 issues they identify, the recent 3 year LTRO may do something to help ease the first two of their concerns, especially in core countries as far as credit conditions go, and at the short end in terms of peripheral sovereign debt spreads, but it will do virtually nothing to resolve the other key issues, and it will not alter the course of the crisis in the longer term. In other words it is not a game changer, even though it will buy time.

But time is – if we look over to Hungary – something we will eventually run out of. Handing over the administration of one country after another to a group of approved technocrats may well work for a while, but it won’t work forever. One day or another, if the measures taken don’t work, Mario Monti will be replaced by the populists, and a new chapter in European history will open. At the present time the policy emphasis on fiscal rectitude and structural reforms, to the neglect of the deep competitiveness and imbalance problems which exist within the Euro Area, is leading us all to no good place. A quick glance over in the direction of Hungary might suggest to us what that place could look like.

Well, that really was the week that was, wasn’t it. It’s over, let it go, there’s another one coming just around the corner, and my initial impression is that it is unlikely to be a quieter or more relaxing one.

On one level, Friday’s news was not really surprising. The French rating downgrade was a shock foretold. As was the breakdown in talks between private investors and the Greek government about a voluntary participation in a debt writedown. A proposition that was unrealistic to start with has been rejected. We should not feign surprise.And yet both events are important because they show us the mechanism behind this year’s likely unfolding of events. The eurozone has fallen into a spiral of downgrades, falling economic output, rising debt and further downgrades. A recession has just started. Greece is now likely to default on most of its debts and may even have to leave the eurozone. When that happens, the spotlight will fall immediately on Portugal, and the next contagious round of downgrades will begin.

Wolfgang Munchau, Financial Times, Sunday 15 January 2012.

Comments are closed.