US economic outlook mixed as manufacturing continues to slow

There’s been a lot of economic data coming out of the US in recent days. None of it shows a clear indication that the economy has turned the corner. Some of the early data on housing was good. But, more recently, the numbers have been murky, particularly regarding credit markets.

None of this says recession. It merely points to continued economic slowing. Nevertheless, I continue to see a 2020 recession as a ‘base case’ due to a lack of policy stimulus. Only when I see clear re-acceleration of GDP growth will I change that view.

Housing

I had thought of posting on this last week before I went on holiday for Thanksgiving because the numbers were really good. Last week’s Mortgage Banker’s Association weekly report showed buoyancy in the housing market due to mortgage rates a full percentage point lower than last Fall.

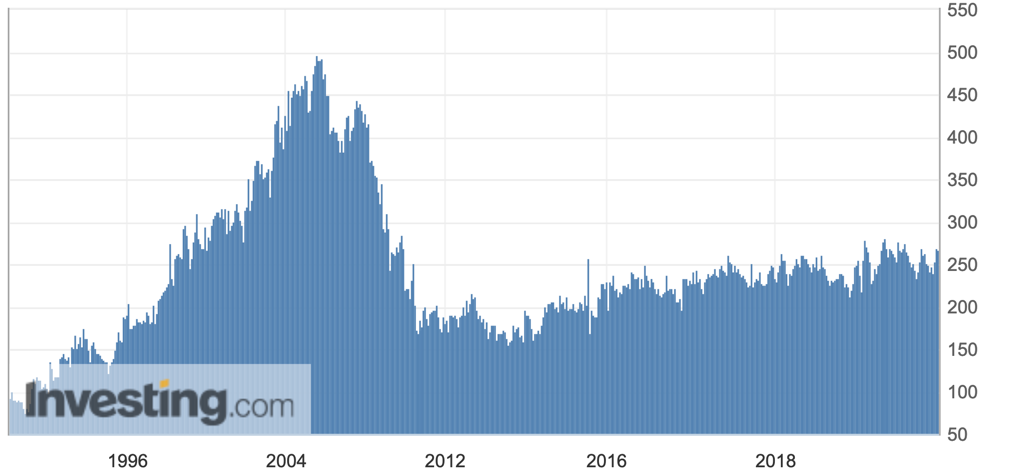

The unadjusted purchase index was at 267.1 versus a year-ago level of 247.8, a rise of almost 8% and in line with the steady rise in purchases since the post-bubble collapse over a decade ago. Here’s what the chart of the US MBA Purchase Index looks like

Source: Investing.com

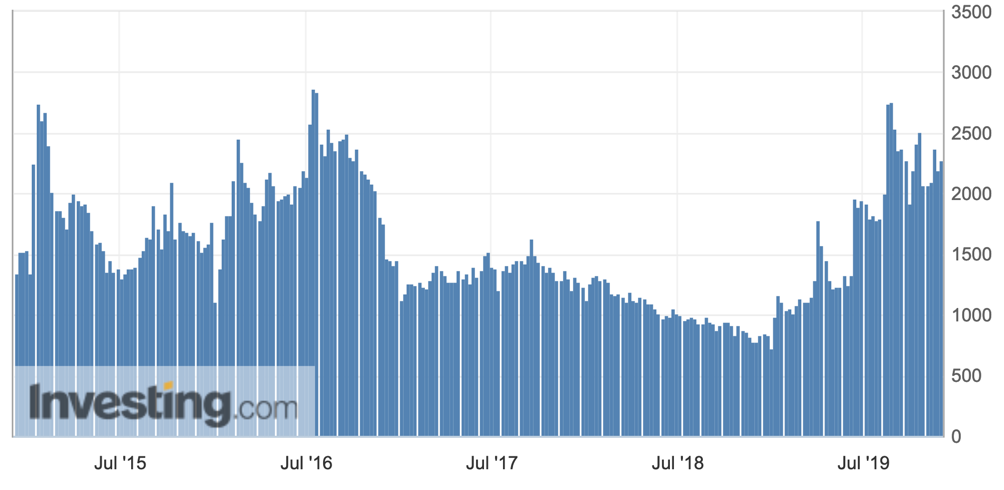

But, for me, it’s the refinancing activity which will give consumers more money to spend and maintain personal consumption growth. That number came in at 2282.2 last week versus a year-ago level of 787.7. So, we are seeing significantly more refinancing activity now than we did a year ago. That’s directly attributable to lower mortgage rates. And the growth in refinancing is more robust than it was during the 2015-2016 cycle. Here’s the chart of the US Mortgage Refinance Index

Source: Investing.com

My overall read here is that we should expect housing to help fuel consumption and GDP growth going forward. And this will act as an anchor against other negative factors building in the US economy.

GDP growth

When you look at the overall numbers, though, they are middling. On Wednesday, the BEA released its second estimate of Q3 growth. And the numbers showed a 2.1% annualized quarterly gain, slightly above the 2.0% gain in Q2.

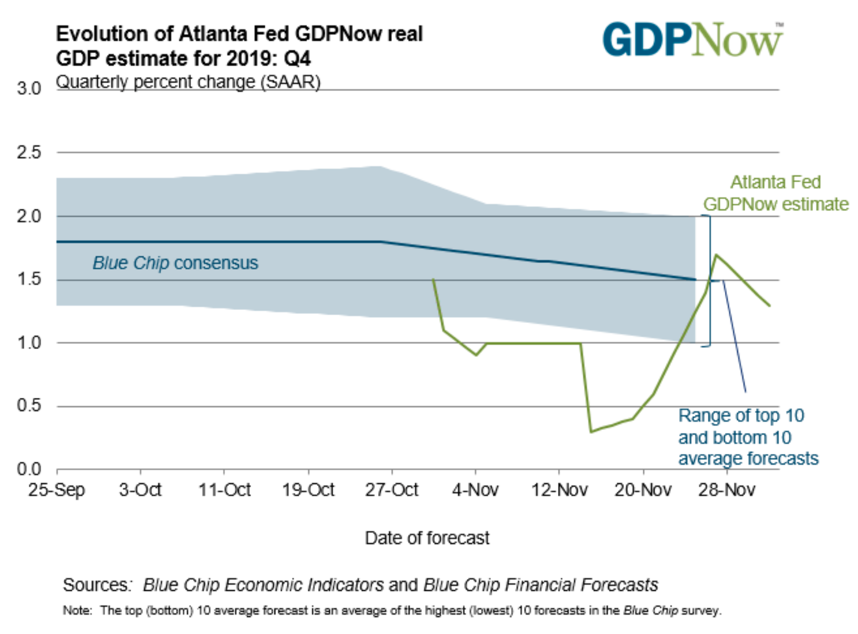

At the same time, the Atlanta Fed’s nowcast for Q4 has increased to 1.3% after falling as low as 0.3% in mid-November.

Source: Atlanta Fed

This is a less alarming picture than a couple of weeks ago. What I see the data saying is that the US economy is slowing gradually. And to the degree the Q4 numbers are above 10%, you could say that we are out of the stall speed range, where an economic shock tips the economy into recession. So, the worry now is not about stall speed itself but that a gradual erosion of growth takes us into stall speed in 2020.

Jobless Claims

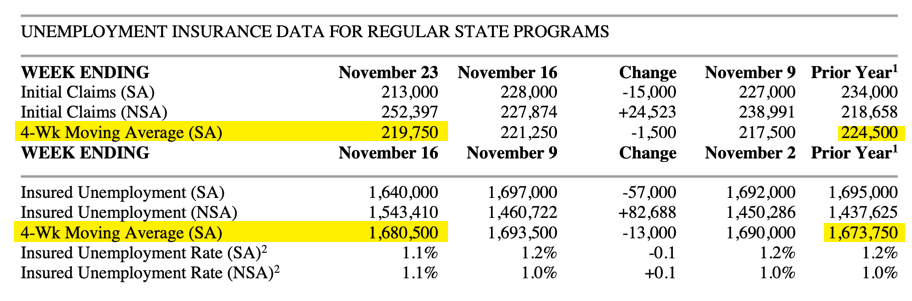

I see the same underlying story looking at jobless claims data. Where a couple of weeks ago, both the initial and continuing claims numbers were above year-ago levels, now just the continuing claims number is. And the number is not that elevated.

For me, this points to a middle ground. The numbers do not suggest recession risk. They point to an economy that is neither accelerating or decelerating rapidly.

And, as I always note, this is a data set I like for real-time feedback. Deterioration in year-over-year levels points to a loss of income that feeds through negatively into consumption. There was a blip where this seemed to be happening. But right now, we’re back on track. Watch these numbers, particularly after the holiday season and early in 2020, for signs of stress.

Manufacturing

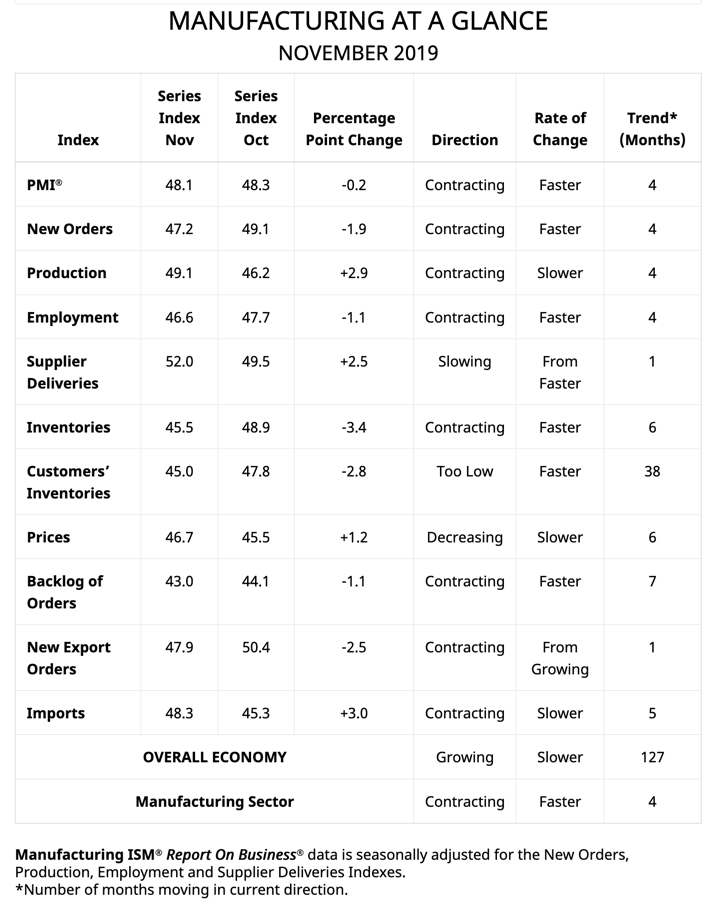

The place where the greatest vulnerability lies in the US economy is still in manufacturing. Numbers released yesterday showed weakness there remains, with the November ISM manufacturing report coming in at 48.1, below 50 for the 4th month on the trot. ISM says their numbers equate to a US economy growing at 1.5%. So we would need to see numbers nearer 45 to become really worried about poor manufacturing data significantly bleeding into other parts of the economy.

If you look closely at the numbers though, what you’ll notice is that production accelerated (perhaps due to the end of the GM strike). But new orders dipped even further, as did employment.

What this says for me is that the US manufacturing sector has not bottomed. We should expect these numbers to decline further still. If the headline figure hits 45, I would be worried that we are at stall speed and vulnerable to recession. Ae’re not there yet. But the direction is down.

Credit markets

I want to end this note with a comment on credit markets. As a former high yield guy, I am keenly aware of how credit and business cycles are joined at the hip. One reason I have been sanguine about the US economy is because credit markets showed few signs of distress. Even though people were alarmed by the Treasury yield curve’s brief inversion between 2 and 10 years this summer, I was a bit less concerned because credit spreads remained low.

But, credit spreads are now creeping up.

If you look at the chart in context, you can see we are nowhere near the distress levels we saw in 2015-16 when the shale boom collapsed. But the numbers bottomed over a year ago and have been going higher since May. These CCC-rated companies are the first ones to default. So it bears watching how this progresses over time, as I think it will be an early warning signal for recession.

My conclusion

So, as we head into the core of the holiday season, the US economy looks pretty good still. Consumption growth remains relatively good. And that growth will be buoyed by the refinancing activity we have seen all year long. Manufacturing continues to be the weak spot. And looking forward, I expect it to get weaker in the near term.

If I had to watch three time series, they would be jobless claims, especially post-Holiday as temporary retail employees get laid off, the manufacturing ISM because a level of 45 is stall speed, and CCC option-adjusted spreads since that’s where credit stress will appear first and most intensely.

Comments are closed.