Can a slowing China tip a stall-speed US into recession?

My last daily post was about the emerging consensus view that a global recession is just around the corner. And the sense I get is that people believe this recession – unlike the one during the Great Financial Crisis – is being stoked by a slowdown in China. And so, the biggest question is whether the US can be tipped into recession because of what happens abroad rather than the other way around.

This is one of the occasional free Credit Writedowns posts I write. If you like what you read please consider subscribing to the weekday newsletter because right now, we are running a limited promotion where you can receive it at a 40% discount.

Scepticism about Chinese data

China is growing at its slowest rate in nearly three decades. And this is in large part because the Chinese authorities have been trying to clean up a bad debt problem. And doing so slows credit growth, which in turn slows economic growth.

But, of course, the quality of Chinese macroeconomic data is wanting. Most China watchers acknowledge that the headline growth numbers are rosy. Here’s Michael Pettis a few days ago, for example:

The Chinese economy is not growing at 6.5 percent. It is probably growing by less than half of that. Not everyone agrees that the rate is that low, of course, but there is nonetheless a running debate about what is really happening in the Chinese economy and whether or not the country’s reported GDP growth is accurate.

The reason for the widespread skepticism is the disconnect between the official data and perceptions on the ground. According to the National Bureau of Statistics, China’s economic growth in every quarter last year exceeded 6.5 percent. While that is much lower than the heady growth rates China has experienced for most of the past forty years, it is still, by most measures, a very brisk rate of growth.

And yet, when you speak to Chinese businesses, economists, or analysts, it is hard to find any economic sector enjoying decent growth. Almost everyone is complaining bitterly about terribly difficult conditions, rising bankruptcies, a collapsing stock market, and dashed expectations. In my eighteen years in China, I have never seen this level of financial worry and unhappiness.

AEI has recently posted on this theme as well.

Look at rate of change data

But, for me, it’s actually directionality that matters most in terms of a slowing or accelerating economy because it tells you where the risks are. And it is clear that Chinese growth is slowing.

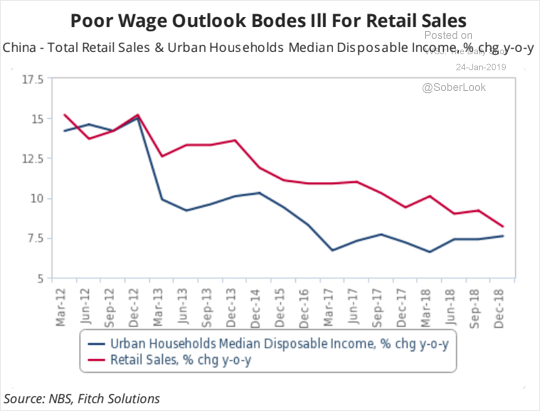

Look at this chart of Chinese wage growth, for example:

It makes sense that nominal retail sales growth numbers would trend down with disposable income. And they are and have been on the downswing for quite some time.

And we should expect this to continue in 2019 as eight of 12 Chinese provinces that have reported 2019 growth targets have revised them downward, according to the South China Morning Post.

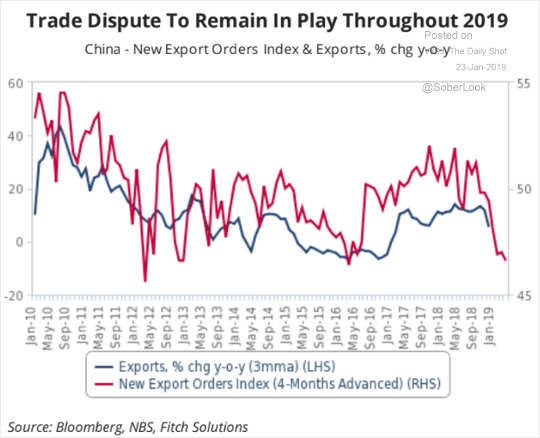

As I said at the outset, the crackdown on bad debt bears some of the blame. But, some of the reason for growth to slow comes from a slowing of external demand as evidenced by trend growth in exports and new export orders.

That’s definitely the trade dispute with the US at work. And I am not expecting a big breakthrough on that front any time soon.

The Chinese solution

The question is what Chinese authorities are going to do about the slowing growth.

On the fiscal side, Chinese Finance ministry officials are saying they will increase fiscal spending in 2019 to support the economy. The focus will be on more tax cuts cuts for small business. And this comes after fiscal spending increased 8.7% last year, despite tax revenue increasing only 6.2%.

On the monetary side, China’s central bank cut the amount of money banks have to hold as reserves five times in the past year. And last week, the PBoC also injected a record $83 billion into the financial system.

On the credit side, yesterday the PBoC set up a central bank bills swap (CBS) to improve the liquidity of banks’ perpetual bonds. The People’s Bank of China said in a statement on its website, this was to encourage banks to replenish capital through perpetual bond issuance. But you have to question both the willingness to go big and the efficacy of the efforts. Chinese officials have repeatedly said that while they would offer more support for the economy, they would not to engage in the “flood-like” stimulus of the past, because of fears of bad debt.

So, while I’m no China expert here, in terms of ‘solutions’, I see further downside risk regarding growth. The good news is that, anecdotally at least, there are foreign companies like Procter & Gamble that say they aren’t seeing the slowdown. And even Alibaba is taking that line. But I trust the rate of change data more. And, in aggregate, those data point down.

Europe will be hit hardest

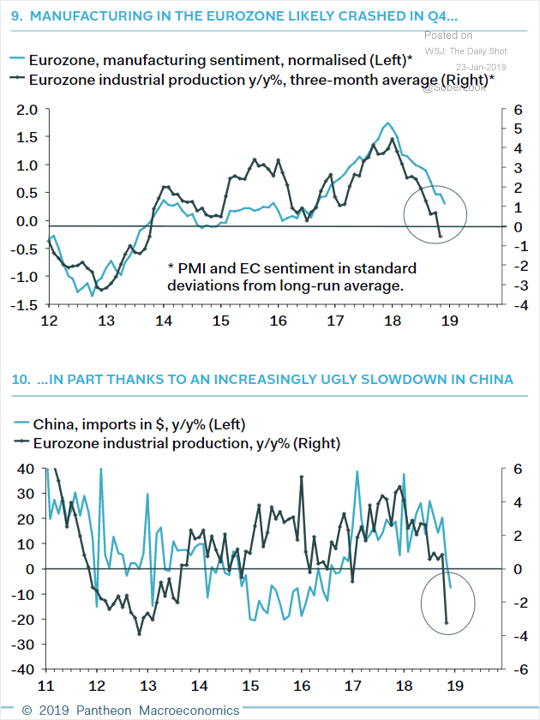

Externally, you have emerging Asia that will see ripple effects from this slowing. But, in the advanced world, my biggest concern is Europe. Back in the pre-crisis days, the euro zone was one giant vendor financing scheme. Surplus countries like Germany sold their wares to deficit countries like Greece and took on credit risk in doing so. When the deficit countries ran aground, the EU put pressure on them to make sure their creditors got their money – lest the creditor country banks went bust.

But, that put huge downward pressure on demand in the euro zone periphery. So, the euro zone creditor countries had to turn elsewhere for incremental external demand. One of those places was China. But, now China is slowing. So, Europe s slowing too. Take a look at the correlation in rate of change data.

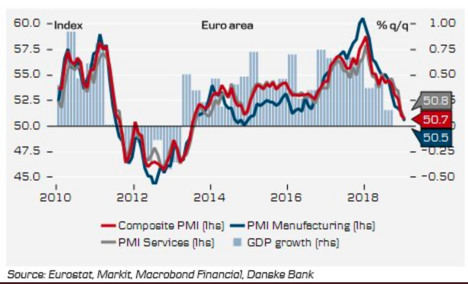

So, business growth in the euro zone has all but stalled in the beginning of 2019. The IHS Markit’s Flash Composite Purchasing Managers’ Index has plummeted to 50.7. That’s the weakest since July 2013 and below even the most pessimistic forecast in a Reuters poll. The median expectation was for a slight rise to 51.4.

And while people are now expecting the ECB to put rate hikes on hold because they acknowledged yesterday that risks are skewed to the downside, I have been telling my investment readers the ECB and all the other major central banks are still too tight. So, monetary policy is not going to lead Europe out of this hole. And fiscal policy is constrained by the stability and growth pact. Europe is in for tough sledding here.

What about the US?

I see the US moving to stall speed shortly, with the shutdown slowdown helping it get there.

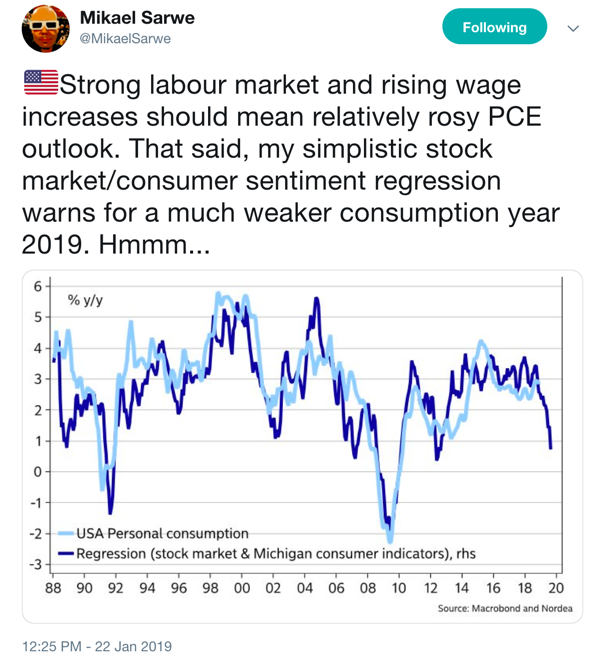

Now, normally I don’t pay much attention to consumer sentiment data because I have not seen numbers that show it is a leading indicator of consumption growth directionality. But this chart – showing a regression of share prices, sentiment and consumption – makes me wonder.

So, I am worried about the trend growth in the US given that we are going to hit stall speed soon. This makes the US vulnerable to exogenous demand shocks from abroad.

What works in America’s favor is the household sector. I think the whole US household sector looks really good right now – not counting the increasing strain from the shutdown. Wages, unemployment, mortgage interest as a percentage of income — there are a lot of things showing resilience in US consumers.

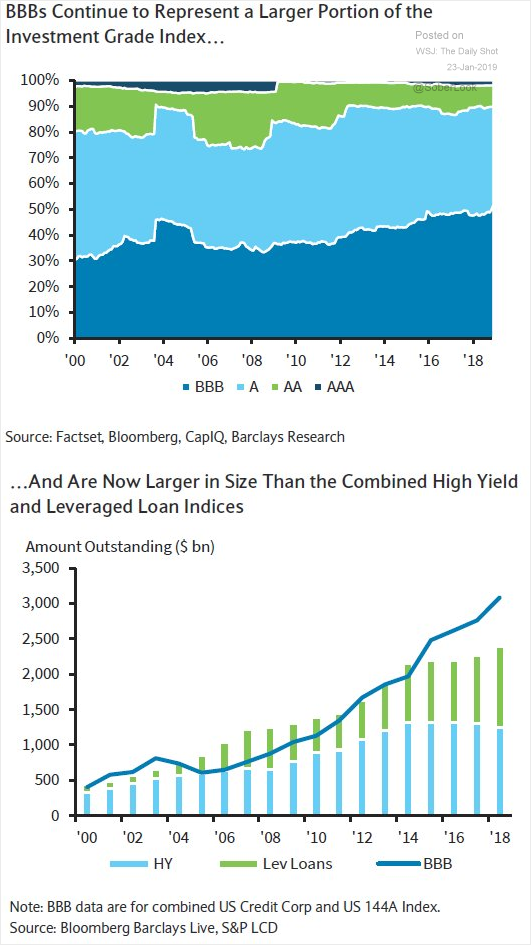

The big problems concerning a global recession are outside of the US and in the US corporate sector, particularly regarding leverage. And you can see that in the increase of BBB-rated securities. That’s where the danger lies because this segment of the credit spectrum is even larger than high yield and leveraged loans combined. And it makes up about half of investment grade US issuance.

My view

Europe is where I expect to see fireworks in 2019, more so than in the US. And that’s because they have low internal demand growth, an excessive dependence on external demand for growth in a world of slowing growth globally and limited policy space with which to deal with those factors.

The US, as a large continental economy, where trade is a lower component of GDP, is in a better position to weather the global growth slowdown. But the risks are mounting. And if the US does fall prey to the Chinese-led global slowdown, it will be the corporate sector that creates the most problems. I am not predicting a US recession any time soon. But, this is no longer an outlier scenario for 2019.

Comments are closed.