My thoughts on the US Q4 2015 GDP numbers

The US economy is not in a recession right now and the latest numbers on US GDP confirm this view. And while the headline growth number was weak, the consumer spending and personal income numbers are supportive of 2%ish growth into 2016. Some brief comments below

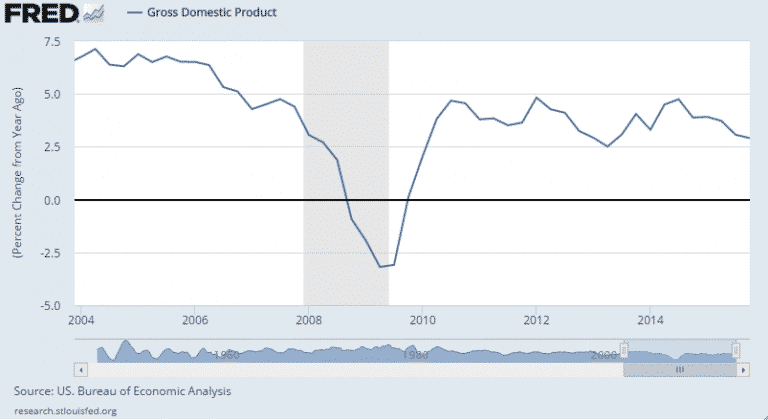

U.S. GDP growth came in at a very weak 0.7% annualized pace for Q4 2015, putting the full year’s growth at 2.4%. Now 2.4% is the same number we had in 2014. And while that is not a stellar number, it is very good by comparison to other large developed economies in the world. For example, everyone keeps extolling the Germans for a job well done. But growth there was 1.7% in 2015 and 1.6% in 2014, weaker than in the US. In Japan, GDP expanded 1.60% y-o-y in Q3 2015. There, the GDP annual growth rate has averaged 2% for the 35 years from 1981 to 2015. That’s what’s happening in the next two largest developed economies.

Underneath the weak 0.7% annualized number are a couple of things to watch. First, there is inventories as inventories reduced GDP -0.5 percentage points in Q4 and -0.7 percentage points in Q3 2015.

We should look at inventories as ‘corrective’ and not core to underlying growth. Ostensibly this is a temporary drag on growth to the degree we are in a mid-cycle pause. However, to the degree that we are nearer the end of the cycle as I believe, then this drag would combine with other factories to take us from stall speed and eventually trigger recession.

On the plus side here, in terms of core underlying growth trends, real disposable personal income has sustained a fairly robust level in the U.S. above 2.5% for over a year now. In Q4 2015, real disposable personal income increased 3.2%. That is the single number that will keep US GDP growth going.

I am less concerned about personal consumption or real final sales numbers to the degree that personal income remains on track. If personal income numbers fall, then falls in consumption are more worrying. “Real gross domestic purchases — purchases by U.S. residents of goods and services wherever produced — increased 1.1 percent in the fourth quarter, compared with an increase of 2.2 percent in the third,” according to the BEA.

The interesting bit here is that the Bank of Japan moved to negative rates overnight, before these data came out. And that caused the Yen to sell off to below 121 to the US dollar. So clearly, the Japanese are now in the same category with the ECB, not just easing but easing quite aggressively via both quantitative easing and negative interest rates. The signals they are sending are that easing will continue indefinitely, with no signs of policy normalization on the horizon. This is US dollar bullish, complicating the Fed’s task.

The stage, therefore, is now set for further policy divergence, with the Fed indicating that an additional hike in March is on the table and that 3 more should be coming in 2016. Nothing in the data released today suggest that I should deviate from a baseline of 2%ish growth in 2016. However, US nominal GDP growth has slowed materially in the time since energy capital expenditures have fallen with oil prices.

And as much as the Fed wants to normalize policy, in a largely deflationary global economic environment where every other central bank is easing, the level of policy divergence we are now seeing is a recipe for serious problems. We should expect further Chinese devaluation, more volatility in commodities and serious downside risk to the 2% growth prognosis for the US economy as a result.

Comments are closed.